Uniformity in income tax rate for all workers |14 January 2011

Effective January 1, 2011, the rate of income tax applicable on the total emoluments earned by a non-Seychellois employee has increased from 10% to 15%.

The new rate of 15% effectively means that all employees, Seychellois and non-Seychellois, will from this month be paying taxes at the same rate.

This adjustment in rate applies to all employees irrespective of salary level or post held, whether you are employed by the private or public sector, or whether you are on a part-time, casual or full-time basis.

Will the salary of non-Seychellois be affected by the uniformity in income tax rates?

The take-home pay of non-Seychellois employees should not change despite the increase in the income tax rate. The increase in rate is a cost to be borne by the employer as part of his total employment cost.

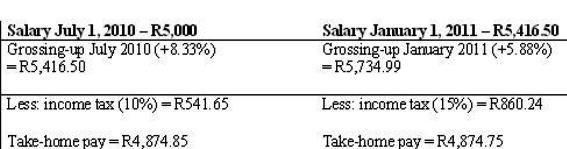

A non-Seychellois employee who was earning, for example, a gross salary of R5,416.50 after the grossing-up in July 2010 will, as from January 1, be given a further grossing up of +5.88% so the take-home pay remains the same after the tax deduction at the new rate of 15%.

Detailed below is the salary working for an expatriate who was earning a salary of R5,000 as at July 1, 2010:

The increase in the income tax rate is in line with Paragraph 3 of the First Schedule in the Income and Non-Monetary.

Benefits Tax Act 2010,while the grossing-up is in line with S.I. 100 of 2010 of the Employment Act.

Have the other rates under the Income and Non-Monetary Benefits Tax Act changed?

It is important to note that all the other applicable rates, as per below, under the Act remain:

• Non-monetary benefits tax payable by an employer is 20%;

• Domestic worker – R50;

• Daycare worker – either R100 or 10% of total emolument whichever is lower;

• A person employed by either a farming company or a boat owner (as defined under the Agriculture and Fisheries Incentives Act 2005) – R100;

• A person receiving an emolument financed by means of an overseas grant under a specific programme or an approved project – 2.5% of the gross amount received.

For more information

If you need further clarification about the Income and Non-Monetary Benefits Tax, please visit the Seychelles Revenue Commission Advisory Centre, Room 2 (Ground Floor), Oceangate House, Victoria, or contact us on the following address:

Seychelles Revenue Commission, PO Box 50, Orion Mall, Victoria. Tel: 293737. Email: commissioner@src.gov.sc

Contributed by the Seychelles Revenue Commission